From information to a plan

You’ve shared your information—now it’s our turn!

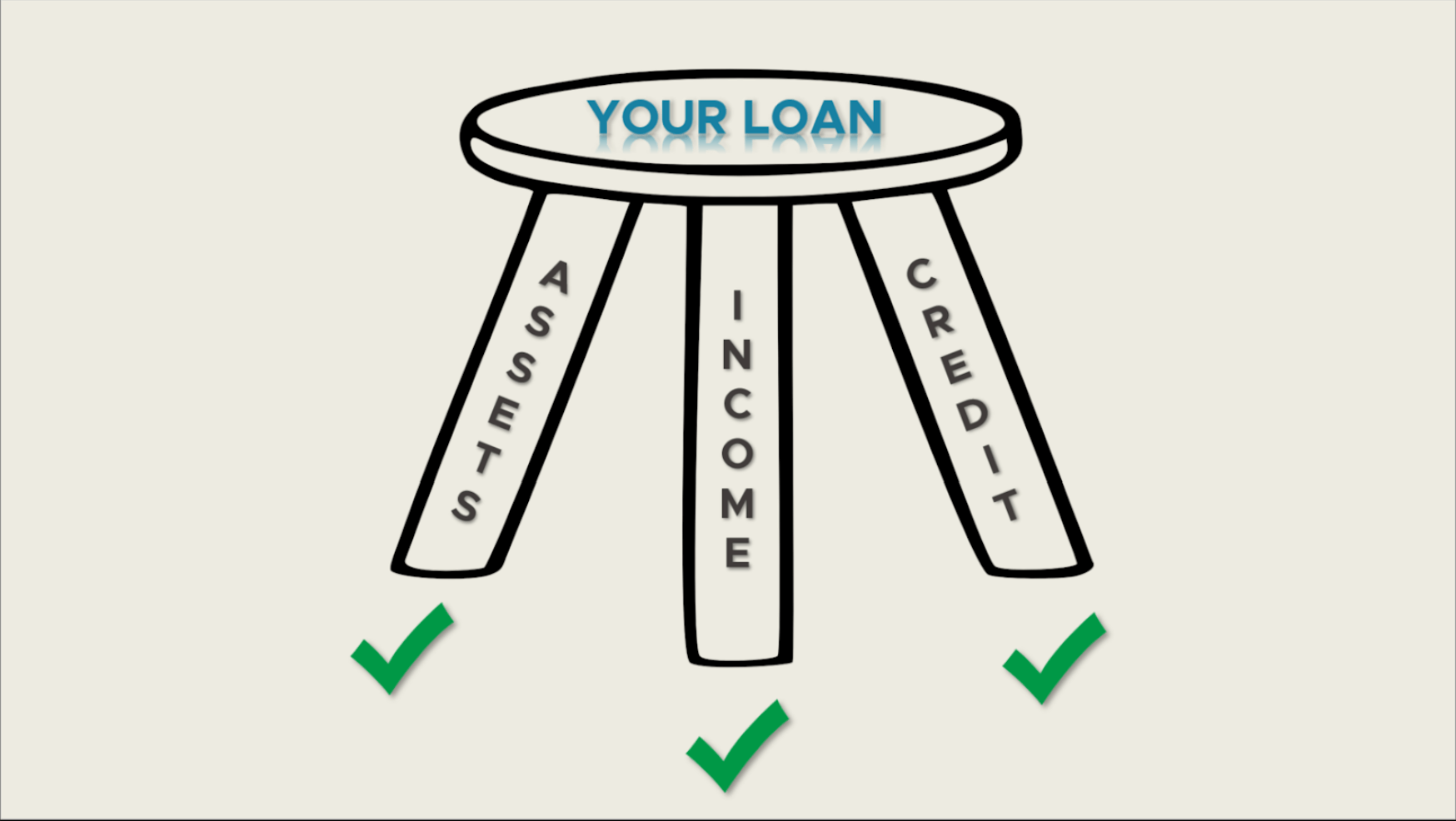

We pull everything together.

We review what you’ve shared and turn it into recommended loan options, actionable insights, and the foundation for your house hunt.

We filter the noise.

We narrow the wide world of loan options to ones that fit your goals and how you’ve told us you want your new home to fit into your bigger financial picture.

We review real numbers.

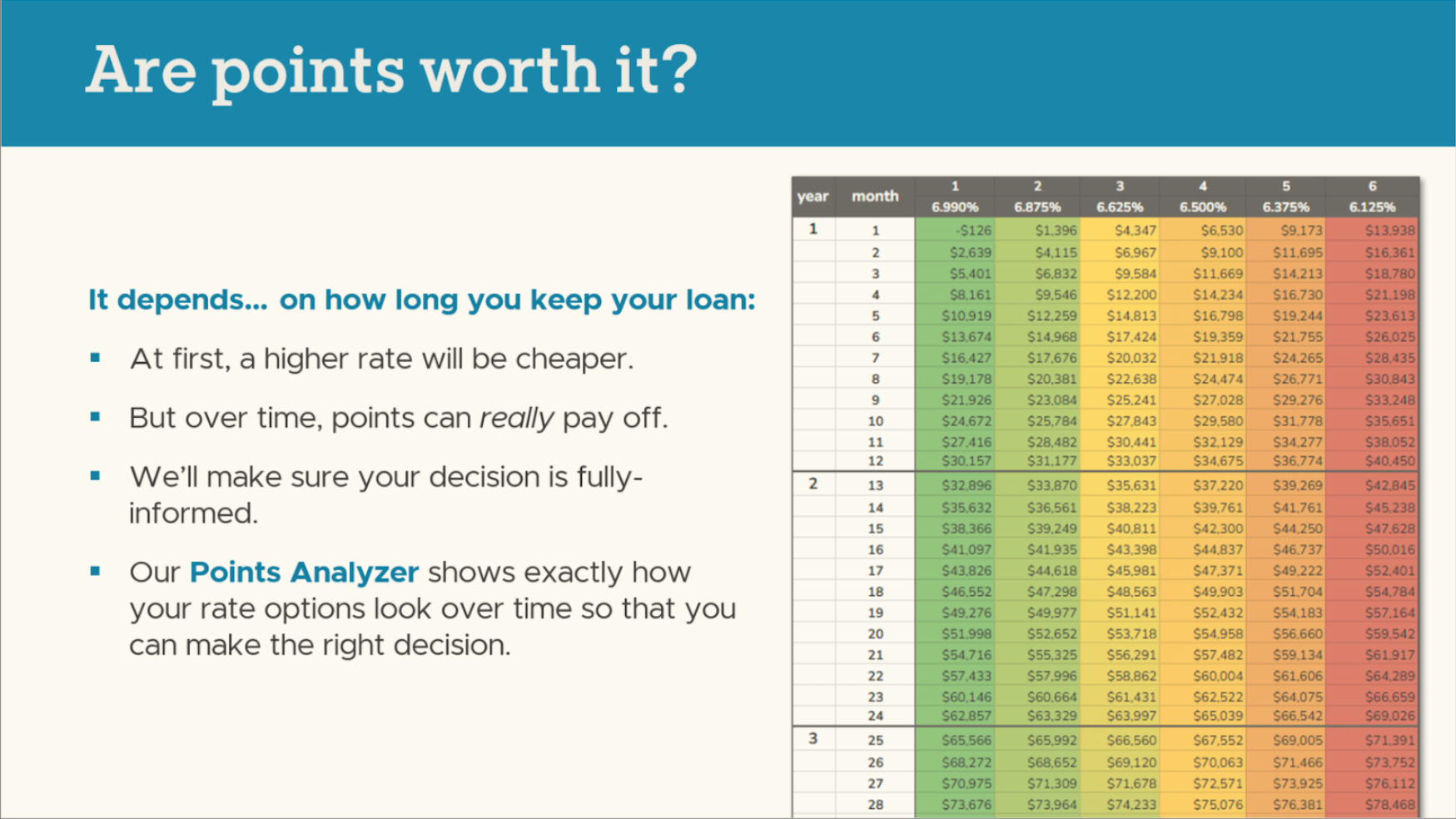

We’ll hop on a virtual meeting to walk through detailed loan options—with real numbers—how each fits your goals, and any trade-offs.

We identify the “known unknowns.”

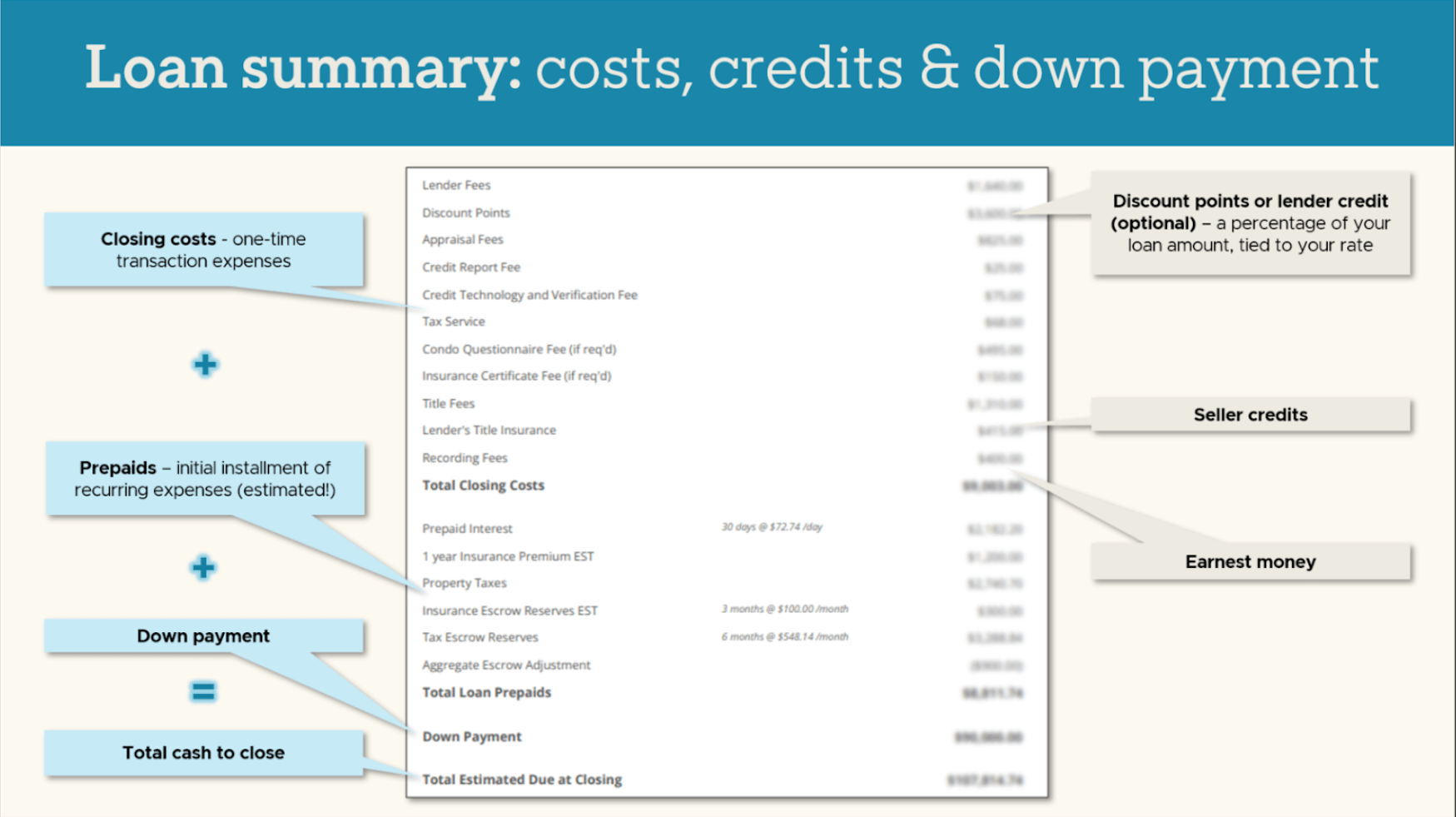

Some details depend on the property. We’ll explain our placeholders, so you understand what could change—and how to connect the dots between homes and numbers as you shop.

We share tips and strategies.

Because this is a meeting for and about you, we’ll talk about ways to optimize loan options, save money where possible, and keep the process smooth and low-stress.

We talk offer strategy.

Loan details only matter once a seller says “yes,” right? We’ll build a toolkit of loan-related elements to strengthen an offer and discuss how best to leverage any seller concessions.

Loan strategy meeting preview

These slides offer a glimpse of the information you may see during our 30–60 minute virtual strategy session. We’ll walk through your personal homebuying math with real examples and connect the dots between the numbers and real properties so that you can shop with clarity and confidence, not guesswork.

This meeting is for and about you, so the specifics vary, but our overarching goal is always the same: whenever you’re asked to make a decision (and there are many along the way), you understand not just the what, but also the why — so every choice feels informed and intentional.

FAQ: loan strategy and the initial planning meeting

What decisions am I actually making at this stage?

Directional decisions—none of which are final.

At this stage, we’re building a clear framework so that when real decisions come up later, they don’t feel rushed or out of left field.

You’ll likely leave this stage with a solid sense of your price range and which loan options best fit your goals — as working assumptions, not final commitments. There’s just too much we don’t (and can’t) know yet.

A helpful analogy might be an old-school darkroom. You start out holding a blank sheet of paper in a dimly lit room. But follow the right steps, and a blurry image slowly emerges, sharpening into a beautiful, crisply-focused photograph.

You probably won’t have that crisp image on day one of a house hunt, but you shouldn’t be in the dark with a blank piece of paper either.

This stage is about understanding how the numbers line up for you, which loan options make sense for your goals, and how different choices affect your buying power, monthly payment, and cash to close — so you can shop with clarity, not guesswork.

Shouldn’t I find a house first and then meet with you?

Definitely not.

We’ll absolutely (also) meet as soon as you find a house. But that meeting should be to fine-tune your financing strategy and firm up property-specific details.

I should add that if the horse left the barn and we need to hustle to get you a pre-approval letter for an offer, we get it—sometimes the house finds you.

But why invite unnecessary stress into your life? Finding the right house is much more efficient (and lots less stressful) when you can use your financial goals as a filter to sort through homes.

Without a clear picture of your numbers, how do you know which homes are a fit? You could break your own heart falling in love with a home outside your comfort zone. When the right home shows up, preparation means you’re not scrambling; you’re ready to act.

And because this whole homebuying project doesn’t get very far without a seller saying “yes”, we’re always thinking one step ahead. We’ll build a toolkit of lending power-ups you and your real estate agent can include in your offer. (Our favorite ones are shiny to sellers at no cost to you. ✨)

How specific are the numbers if I don’t have a house yet?

We like to think of them as specific hypotheticals. That may sound like an oxymoron, but stay with us.

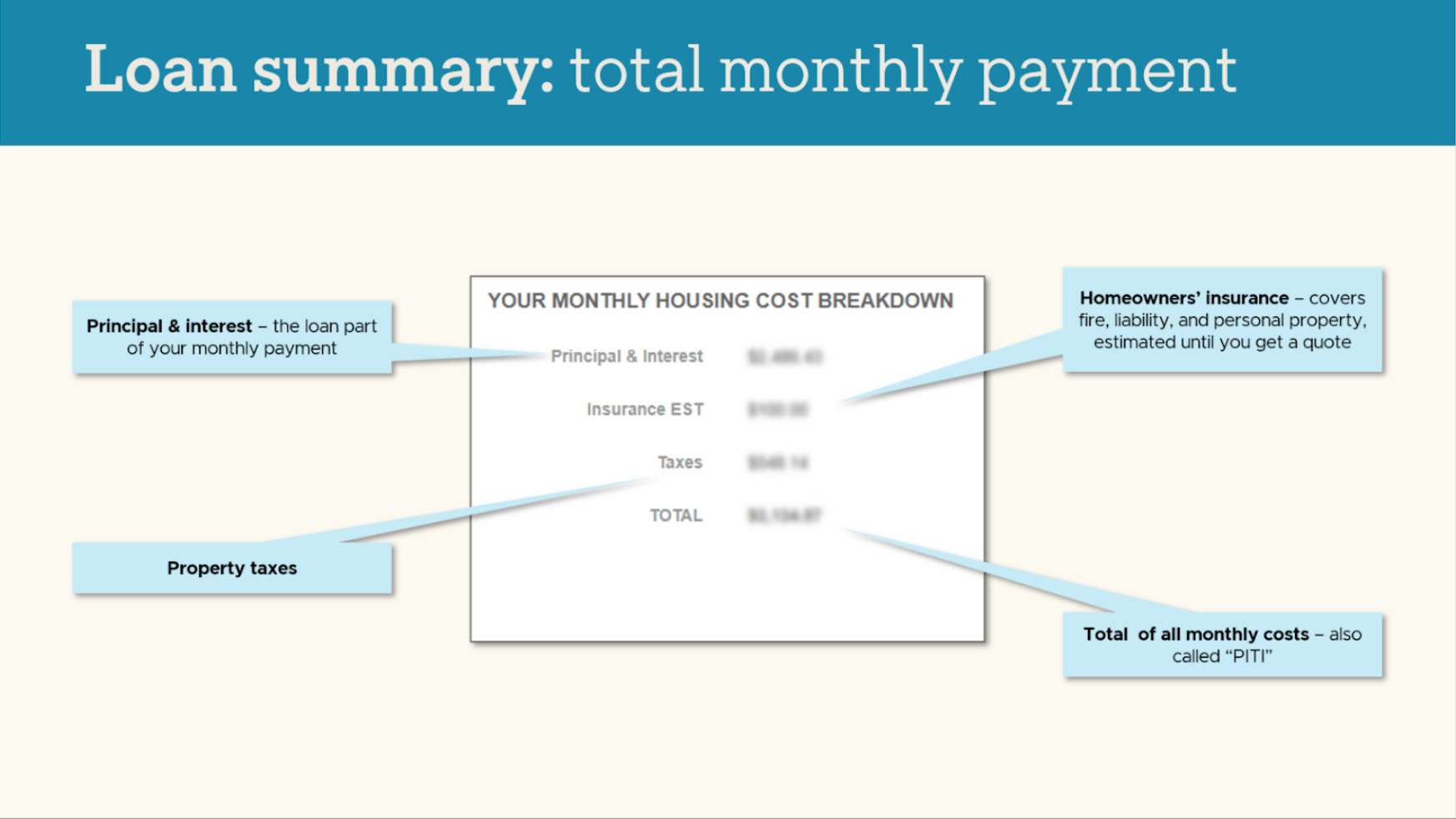

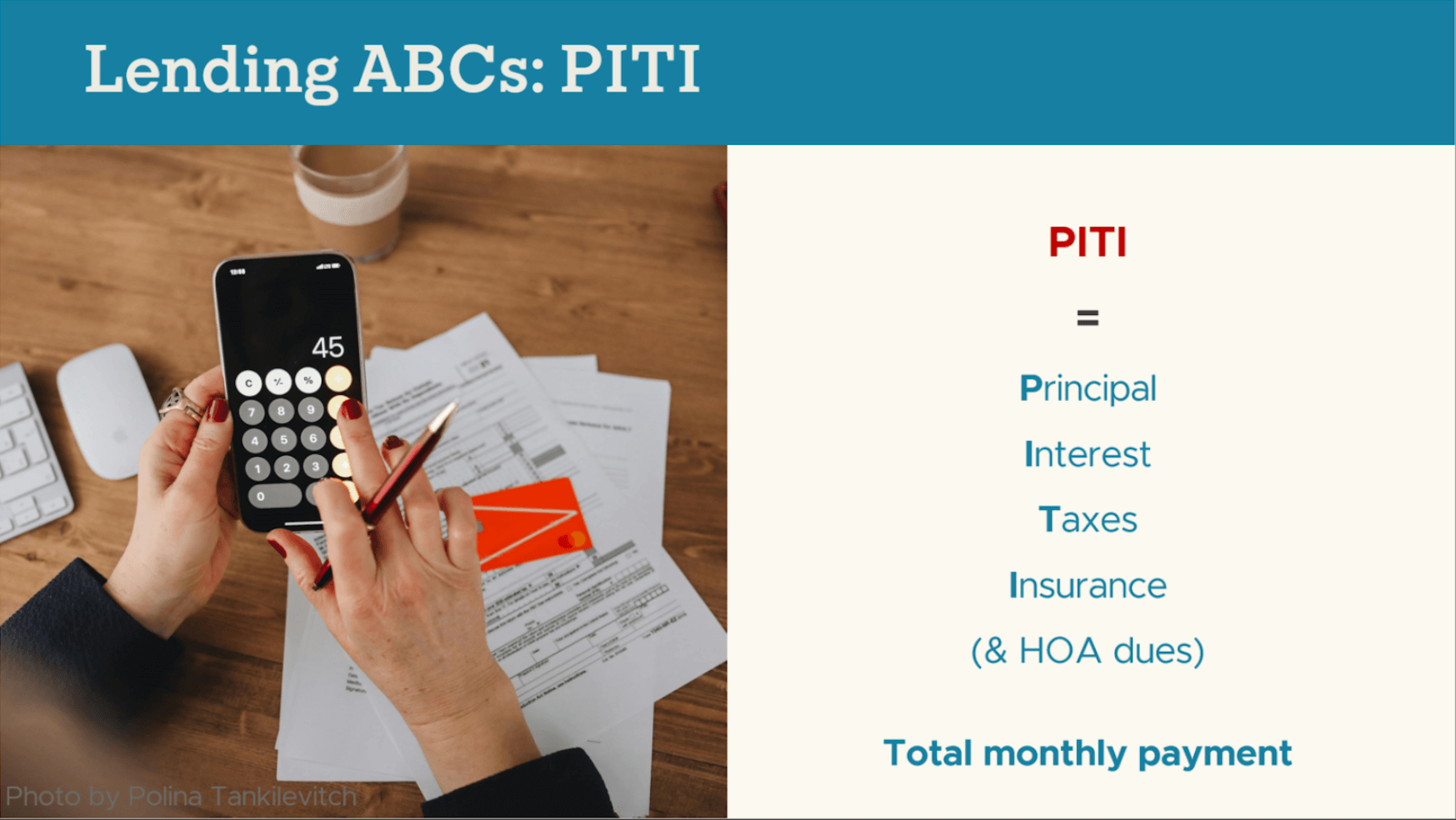

A house hunt starts with many known unknowns. How much will property taxes and insurance be? Will there be any HOA dues? Will interest rates change before you buy? Even the final price of your home is TBD.

If you already know these things before you start, please lend us your crystal ball. Otherwise, we’ll use placeholders tuned by our years of experience.

We’ll be clear about where we’ve made an assumption, do our best to err on the safe side, and call out places where the margin of error may be higher.

And then—if you’re game—we’ll have a little fun with the numbers. “Fun” and “numbers” don’t always pal around together, but we’ll share a few handy rules of thumb that allow you to quickly compare and connect properties to numbers in your head (or on your phone).

When it comes to the numbers, you’re never on your own. We’re always available to whip up numbers when you’re considering a property. But shopping is more fun when the numbers don’t feel random or like guesswork.

Will you show me more than one loan option?

Signs Point to Yes. 🎱 But always with intention.

In a sense, we’re matchmakers. You share your goals and financial resources, and we filter the wide world of loan options down to the ones that best fit. When comparing options, we’ll clarify the tradeoffs and explain how each aligns with your priorities. Side-by-side comparisons are a tool we find especially helpful.

That said, we don’t believe in overwhelming you with information about every possible loan just because it exists. If you’ve heard about an option we didn’t mention, just ask—we’re always happy to explain why it didn’t rise to the top of our list.

And sometimes, there’s clearly the One Best Fit. When that happens, we’ll explain why. Strategy matters more than menus.

What happens if my priorities change once I start shopping?

It would be unusual if they didn’t.

One of the reasons we like to meet and talk through loan options and numbers early is to help you understand how changes in priorities might affect the bigger picture. As you shop and get a better feel for what’s on the market, your needs and wants will naturally evolve.

Think of your initial loan strategy as a flexible framework — something you can test different properties and shifting priorities against. As your house hunt unfolds, we’ll revisit assumptions, update numbers, and adjust the strategy as needed, so your financing continues to align with your priorities.

Do we have to meet before getting a pre-approval letter?

Nope! (But we really hope you will.)

If you’ve already found the home and need a quick pre-approval letter, you’ll be pleased at how quickly we can make the magic happen. 🪄

But when we’re talking about best practices, meeting to review your loan options and numbers before you start house hunting is high on our list.

It would be quicker and easier for us to email a pre-approval letter and wish you luck. We’re always looking for ways to be efficient, but this just isn’t the place to cut corners. There’s no shortcut to the clarity that comes from going over numbers together, answering questions in real time, and walking through “what-if” scenarios.

It’s a 30–60 minute conversation up front that prevents surprises later and sets the stage for confident, intentional decisions throughout the process.

Is this different from a typical pre-approval?

Yes and no.

In our view, taking time to discuss loan options and real numbers is a critical step that no buyer — and no lender — should skip.

That said, practices vary widely. Many pre-approval letters are written with minimal conversation, which can (intentionally or unintentionally) skip discussions about numbers and details of loan options that are, you know, kind of important.

Issuing our clients letters and just sending ‘em out to shop would be quick and easy. But we’re committed to an educational, strategy-driven process because we believe it leads to better outcomes.

(Also, we’re big nerds for what we do and can talk about mortgages all day.) (Oh, wait. We do talk about mortgages all day.)

We want you to understand how each loan option works, why you might choose one over another, and how those choices connect to properties—and to your life. Your home should complement your life and the people and priorities that matter most to you.

Every part of our process is shaped by decades of experience, focused on helping you navigate the big, financially impactful decisions that come with buying a home… with clarity, context, and calm confidence.

Explore our PDF library…

We have a library of downloadable PDFs, exploring loan programs and explaining some of the more mystifying parts of the mortgage process.