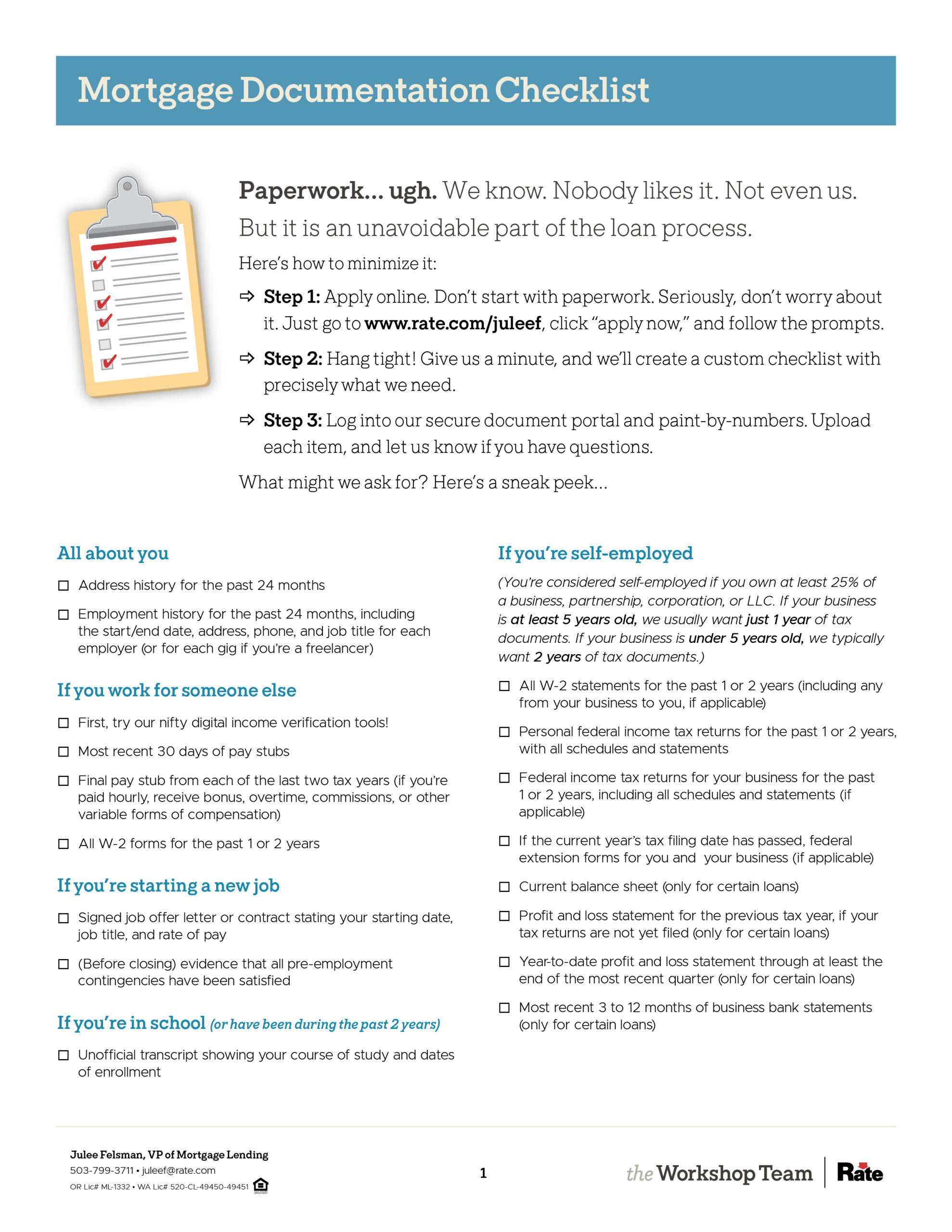

You know that scene in The Matrix? The one where everything slows down and Neo can dodge bullets? Let’s turn you into Neo. (Trenchcoat optional.)

With a few simple (and mostly common-sense) tips, we can help you help us help you (😝) dodge common lending hazards and pave the way to a speedy, smooth, stress-free mortgage process.

So please read through these practical tips. And don’t skip the “asset” section—you’ll find it especially rewarding. (Hint, hint. 😉)

(Prefer a PDF to read offline? Download that here.)

Pro tips: Timing & Communication

Pro tips: Your Whereabouts

Pro tips: Documentation

Pro tips: Employment & Income

Pro tips: Assets & Money for Closing

Pro tips: Credit & Debts

Pro tips: Legal & Tax Matters

Pro tips: Homeowners Insurance

Pro tips: Et cetera, Miscellany & Sundry

Connect with us on YouTube…

We have a growing YouTube library of videos covering every part of the mortgage process. Head over and explore, and don’t forget to subscribe (and turn on notifications so you don’t miss new videos!)