Your new processing friends…

This is detail oriented, specialized work, so we’ll be introducing a new primary point person.

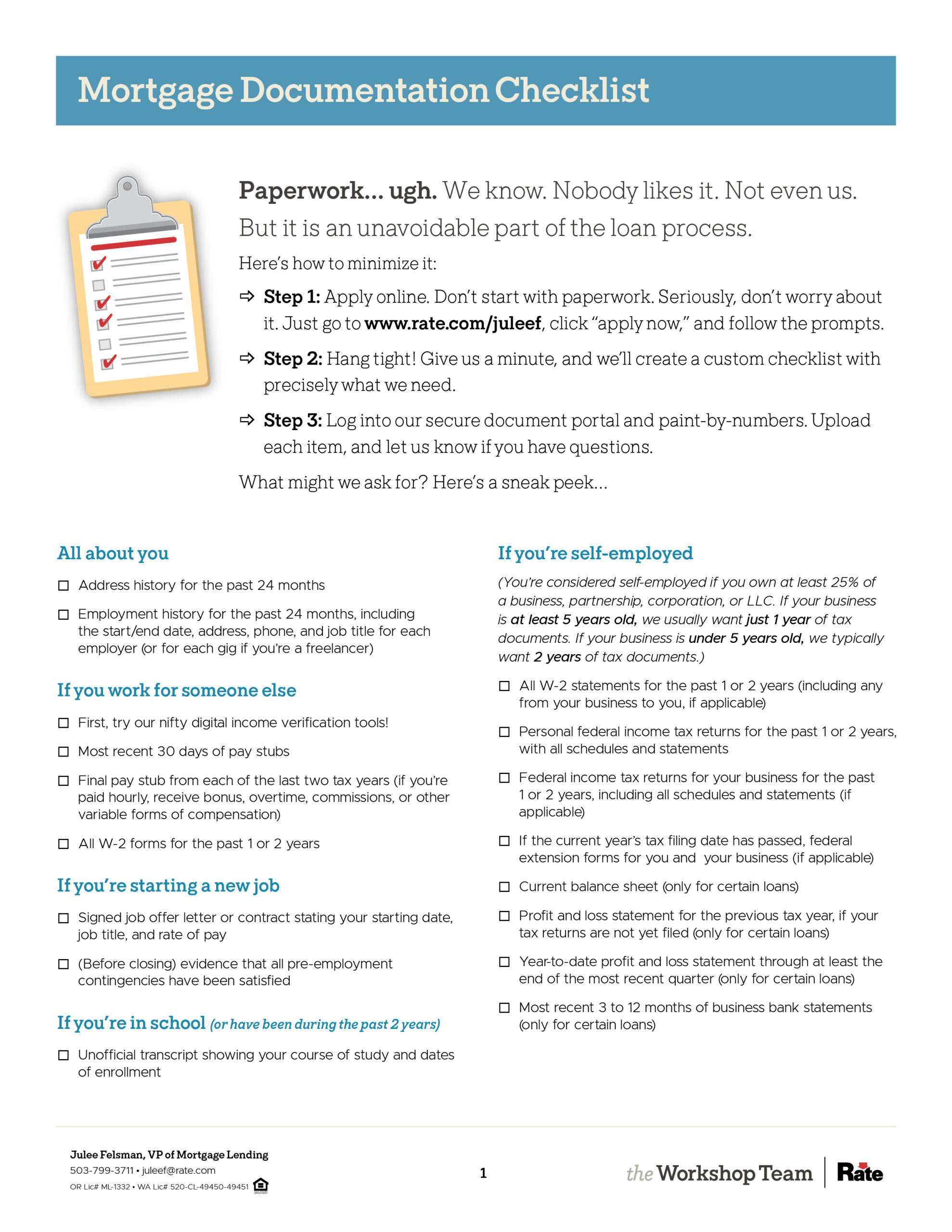

3 things to know…

We’re on your side

Whoever takes the lead, their job is the same: to review everything you’ve already shared with us, update your task list with any needed items for processing, and organize everything for underwriting.

Timing is important

Please complete tasks within a day or two to keep things moving smoothly. The resources on this page are here to help answer common processing questions, but don’t hesitate to reach out if anything feels unclear.

Questions? Reach out!

Our processing team is ready to assist, and your loan partner is still your go-to for anything related to loan numbers and details. Let’s work together to keep the momentum going!

FAQ: mortgage processing

Welcome to processing! Sounds bureaucratic, doesn’t it? (We should have workshopped the name a little more.) Below, I’ve compiled answers to common questions as we make our way through processing on our way to the main event — underwriting and loan approval.

Introduction to Mortgage Processing

What is mortgage processing?

Processing is where we update, gather, and organize your information and paperwork so that an underwriter can review and approve your loan.

Why does processing feel like a repeat of pre-approval?

It’s deja vu all over again. (Kinda.)

Processing starts with the information you provided during pre-approval but takes it further — updating and expanding on it. Every document in your loan file has a “sell by” date. During processing, we’ll update anything that’s expired.

At pre-approval, we take a “less is more” approach. We gather just enough information to determine the best loan options and confirm your eligibility. But, loan guidelines are full of nit-picky details that we must address before closing.

Maybe you took a few months off to spend time with a new addition to the family. During pre-approval, we’ll note the break and ask you about it. In processing, we’ll ask for a short letter explaining the gap.

Or perhaps a generous aunt is helping with your down payment. We’ll plan around the gift during pre-approval and while you shop. Our processor will guide you through documenting it.

Our processing team is here to guide you through these important housekeeping items.

What’s the difference between the processing and underwriting?

Processing is preparation for underwriting.

Processing involves gathering, organizing, and verifying documents and information.

Underwriting is where an expert in loan rules reviews this information, confirms it meets loan guidelines and issues approval.

How long does the processing take?

Ideally, as little time as possible. A typical cadence might look like this:

Day 1 – The processor reviews your file and requests any additional information or documentation required.

Day 2 – You gather and provide the items requested.

Day 3 – The processor reviews what you’ve shared, verifies that all necessary information is in place, organizes everything, and submits your loan to underwriting.

But we may hustle to move faster if you’ve written an offer with a quick closing date. And, of course, some information and documents might not be available on short notice. Get us everything available quickly, and keep us posted on loose ends.

What should I do if I forgot to mention something about my finances?

Please fill us in right away! This isn’t the time to keep secrets or hope something won’t surface. Underwriters are thorough, and anything omitted can slow things down.

Plus, at closing, you sign paperwork saying everything you’ve shared is accurate and complete.

Keep your friends in processing posted, and we’ll work with you to document every element of your financial picture and keep things moving forward.

I’m still negotiating with the seller. What if the price changes?

That’s okay! Continue with the loan paperwork while you hammer things out with the seller.

If anything changes — like the price, loan amount, a rate lock, a seller credit, or anything else — we’ll update our file and send a minty fresh Loan Estimate reflecting the changes. (Maybe not minty.) (But scratch ‘n’ sniff loan documents are an interesting idea.)

What if there’s an error on the application or missing information?

Let us know!

Stuff changes…and a few months may have passed since we set up your pre-approval. If anything is out-of-date or otherwise inaccurate, fill us in.

But, don’t get too hung up on the minutia…yet.

Your application is a living document that evolves as we process your loan. We update it as we gather new or more recent information. You’ll sign the final, fully updated version at closing.

Bank, investment, retirement, loan, or credit card balances are a moving target. We want to know if something significant has changed, but normal fluctuations are expected.

Our forms are always a snapshot in time. Bank, investment, and retirement account balances reflect the most recent on a statement or digital asset report. Loans and credit cards reflect the balance shown on your credit report.

Why are you asking me to waive my right to receive a copy of the appraisal?

We’re not. 😔 If the ECOA Valuations Waiver isn’t the most confusing document in lending, I don’t know what is.

We’ll send you the appraisal no matter what — it’s the law.

However, there’s a mandatory 3-day waiting period between receipt of the appraisal and the earliest day you can legally sign closing documents.

This waiting period applies to every part of the appraisal, and two things sometimes slide in close to closing:

Corrections: Underwriters often ask for clerical corrections. If the appraiser is busy or on vacation, these may roll in close to closing.

Repairs: If a contractor takes until close to closing to complete a repair, the appraiser’s time may be limited to re-inspect and verify completion.

Checking the middle “Election” on the ECOA Waiver form waives the waiting period and allows signing within 3 days of receiving any element of your appraisal.

Why are you pestering me for small, irrelevant things when I’m obviously good for the loan?

We’re so annoying. But please don’t shoot the messenger. The real culprit? The SEC.

Here’s how the modern mortgage marketplace works:

When you close on a mortgage (in what we call the “primary transaction”), you get money to buy your home, and we get a “promissory note” — your promise to repay $X at Y% over Z years.

It’s a valuable piece of paper (glance at a mortgage amortization schedule, and you’ll see why) (you’ll pay lots of interest to the noteholder).

But there’s a catch for lenders — we only have so much money to lend. Once we run through our funds (no matter how valuable our stack of promissory notes), we’re done as lenders.

The solution to this problem is the “secondary market.” Lenders can sell bundles of loans to investors like Fannie Mae and Freddie Mac. They repackage the loans into bonds and sell them as Mortgage-Backed Securities (MBS).

Here’s where the SEC comes in. To give investors confidence and transparency around what they’re buying, every loan destined to be part of an MBS pool must meet standardized guidelines. The nit-picky requirements are a byproduct of creating predictable, consistent, low-risk investment-grade bonds.

So, when we bug you for small, seemingly irrelevant things, please bear with us. And there are silver linings:

For us…job security!. Someone’s gotta collect all of the paperwork, dot every ‘I,’ and cross every ‘T.’

For you…access to long-term, (relatively) low-interest mortgages. Thanks to this system, your mortgage is a liquid, fungible commodity traded globally, and the U.S. is the only country where 30-year fixed-rate loans are the norm.

Processing Timelines & Staying on Track

I’m busy with inspections, can’t this wait?

It depends. We always have one eye on the clock (or calendar). The time we need to get your loan closed varies, but here are general guidelines:

If closing is three weeks away or less, we need to keep moving. Send conditions to our processing team as soon as possible—ideally within one to two days. Hitting “pause” delays submission to underwriting and could create a domino effect that results in missing your closing date. If the seller doesn’t agree to an extension, your purchase and earnest money could be at risk.

If closing is four weeks away or more, you may have time to focus on inspections before resuming work on your loan. But… we’d still love to have you chip away at the processor’s requests. Holding off can artificially compress timelines leading to more time pressure later.

Allowing us to proceed with processing while you hammer out the details with the seller doesn’t lock you into anything. We’ll do our thing behind the scenes and hope for the best. When things are a “go,” we’ll be moving along at a good pace. If you hit an impasse and decide this isn’t the right house, we’ll hit the brakes and wait for you to find the home that’s meant to be yours.

What happens if I’m slow to provide documents to processing?

The mortgage process is linear — like a train rolling down a track, stopping at different stations along the way. Processing is meant to be a brief stop before we head to underwriting — where your loan gets approved.

Delays to providing documentation can put our train behind schedule. Playing catchup requires rushing through subsequent stages or maybe even missing your closing date.

If there’s something you’re struggling to find or need some extra time to chase down, let us know. We’ll work with you to keep things on track (or adjust timelines, if necessary).

Submitting Documents to Processing

Is it safe to upload my documents to your portal or the Rate app?

Yes! Our portal and the Rate app are encrypted and secure.

We’re legally obligated to protect your personal and financial information both as you send it to us and as we store it. But more than that, we feel obligated to treat your information and documents how we’d want our own treated.

How do digital asset verification tools work?

Our digital asset verification tools securely verify your bank information — with no statements required!

Here’s the process:

• Log in to our portal.

• Look for the task to “Verify assets automatically.”

• Click it and search for your bank, credit union, or other financial institution.

• Connect your account.

• Click “Submit” to share with us.

• Repeat for as many accounts as you’d like.

We can’t see your username or password and don’t have access to your account. We just get a report that eliminates the need for you to provide statements for the accounts you connect and share.

We can refresh the report during a 60-day window, which may eliminate requests for other documentation—like proof that your earnest money has cleared your account, receipt of a gift, or transfer of funds.

As a bonus, if you’re on direct deposit at work, we may be able to verify your income, crossing even more paperwork off of your to-do list.

We offer this service to streamline the process and eliminate paperwork, but it’s not mandatory. If you’re uncomfortable connecting your account or some of your financial institutions aren’t eligible, we can document everything the traditional way with bank statements.

Should I send everything to processing at once, or can I send things when they’re available?

It’s not only okay to share items and information as they become available – I’d even encourage it.

Sending documents piecemeal is less satisfying than crossing everything off your list at once, but it gives our processor a chance to review things as soon as possible.

Some documents lead to additional questions or extra paperwork. It’s annoying when that happens, but navigating when we’re not pressed for time is much easier.

This is a great time to suggest that you read Help Us Help You. It’s full of suggestions for avoiding avoidable paperwork — and there’s a Secret Toy Surprise. Read it and claim your reward!

Can I email documents to processing?

You can, but we don’t recommend it. Email is vulnerable to being intercepted en route or accessed if someone hacks into your account. For security, please upload documents to our web portal or the Rate app.

Can I take photos of documents?

You sure can! Photos are just fine as long as they’re legible and include the entire document, from edge to edge. Here’s a checklist for photographing documents:

• Position yourself with a bright light source in front of you to avoid shadows. A table in front of a sunny window works nicely, but a desk lamp also works well.

• Hold your phone directly above the document so the document is as square as possible.

• Position your phone so that all four corners of the document are visible.

• Take a photograph of every page (even pages without any information) – including the front and back of double-sided documents.

• After taking each photo, zoom in to ensure the letters and numbers are legible.

• If you have trouble getting clear photos, consider using a scanning app like Adobe Scan, Microsoft Lens, or CamScanner.

You can securely upload images from your phone using our web portal or the Rate mobile app.

Can I take screenshots of documents?

Probably not. Screenshots or photographs of your computer screen rarely include the necessary ingredients for mortgage underwriting — your full name, the account number, beginning and ending balances, and itemized transactions covering a 60-day period.

Once you’re logged into your financial institution’s website (or payroll portal), look around for a link to “documents” or “statements.” Sometimes, the best way to get a PDF you can upload to our portal is to click on a link to “print” a document – the printer-friendly version is usually a PDF version of a statement, just like you’d get in the mail. You can save and upload it (no need to print and scan).

If we ask you to document a transaction after the most recent statement, this document explains how to create a transaction history that satisfies underwriting requirements.

Do I need to print and scan documents, or can I use my phone?

You can absolutely use your phone to take photos of documents or use scanning apps like Adobe Scan, Microsoft Lens, or CamScanner.

Will I need to pay for anything during processing?

Yes! Our processor will ask you to pay a deposit for our application fee ($150), your credit report ($30 per person), and the estimated cost of the appraisal ($500 to $900, depending on the location and type of property you’re buying). These are part of your closing costs, so paying them now reduces the amount due at closing. You’ll see them marked “paid outside of closing” (POC) at the closing table.

Income Documentation for Processing

Will you need my income tax returns?

Maybe. If you’re freelance or self-employed, have rental, retirement, investment, royalty, or other non-wage income, we’ll likely need your most recent 1 or 2 years of tax returns.

Some first-time buyer programs require 3 years of tax returns as evidence you’ve not owned a home.

But if all of your income comes from a good old-fashioned job, we’ll probably document it with pay stubs and W-2 statements—no tax return required.

Should I hurry to file last year’s tax return?

Probably not… but talk with us! If we used a prior year’s tax returns to pre-approve you, filing a new tax return may change your loan qualifying income. A change to your income (up or down) could affect your loan approval. Talk with us before filing a new tax return!

What if last year’s tax returns aren’t filed yet?

If it’s past April 15th (or another filing deadline for you or a business), we’ll ask for proof you’ve filed for an extension (Form 4868 for personal tax returns or Form 7004 for a business) and proof you’ve paid any estimated taxes due. We’ll also request copies of any W-2s, 1099s, or K-1 statements.

What paperwork do I need to document my income?

The documents we need depend on the source of your income. Here’s an outline of what you can expect us to ask you to corral:

Income from employment (workin’ for “the Man”):

• 30 days of pay stubs.

• Most recent 1 or 2 years of W-2s.

• If your income is variable (overtime, bonus, commission, shift differential), the last pay stub you received at the end of the previous 1 or 2 tax years.

• If you’ve filed an extension for the most recent year of tax returns, we’ll want a copy of the extension form.

• But sometimes… we won’t need anything from you! (We have digital tools that may document your income automatically.)

If you’re self-employed and file as a sole proprietor (all of your business income and expenses show up on your personal tax return):

• Most recent 1 or 2 years of personal federal tax returns with all schedules and statements.

• If you’ve filed an extension for the most recent year of tax returns, we’ll want a copy of the extension form.

• For some loans, a profit and loss statement beginning when your last tax return ends and running through the end of the most recent quarter.

• For some loans, a current balance sheet.

If you own 25% or more of any business entity (Partnership, S Corp or C Corp):

• Most recent 1, 2, or 3 years of W-2 statements from your business to you.

• Most recent 1 or 2 years of personal federal tax returns, with all schedules and statements.

• Most recent 1 or 2 years of federal tax returns for your business, with all schedules and statements.

• If you’ve filed an extension for the most recent year of personal or business tax returns, we’ll want a copy of the extension form(s).

• For some loans, a profit and loss statement beginning when your last tax return ends and running through the end of the most recent quarter.

• For some loans, a current balance sheet.

If you earn rental income:

• Most recent 1 or 2 years of personal federal tax returns, with all schedules and statements.

• For property that doesn’t appear on your most recent tax returns, a copy of current leases.

If your compensation includes Restricted Stock Units:

• RSU grant agreement(s) and vesting schedule(s).

• The last pay stub you received and the end of the previous 1 or 2 tax years.

• Most recent 2 monthly brokerage statements for the account associated with your RSUs.

For retirement or investment income, the paperwork depends on the source:

• Most recent award letter for any pension or social security income.

• Most recent 1 or 2 years of 1099 forms.

• Most recent 1 or 2 years of K-1 statements for any businesses in which you have a less than 25% ownership interest.

• Most recent 2 monthly (or one quarterly) statement(s) for retirement and investment account – all pages of each.

Not sure what to gather? Don’t worry! We’re here to help and can walk you through exactly what’s needed to document your income.

Asset Documentation for Processing

What are “assets”?

Assets are anything you own that has value. However, for mortgage lending purposes, we typically only care about financial assets and real estate.

Financial assets

• Checking, savings, money market, and credit union accounts.

• Certificates of deposit and savings bonds.

• Brokerage accounts with stocks, bonds, EFTs, and mutual funds.

• Retirement accounts, like 401(k)s and IRAs.

• Life insurance policies with cash value.

• Annuities.

Real estate

• All properties in which you have an ownership interest – whether they’re your primary residence, a vacation home, or an investment property.

Non-financial assets like personal property, collectibles, precious metals, and vehicles are only relevant if you sell them or fund your down payment with a loan that uses them as collateral.

We only need to document crypto-currency if you plan to liquidate it.

Keep us in the loop regarding the funds you’ll be tapping into, and we’ll guide you through the required documentation.

What paperwork do I need to document my assets?

We can document assets for the mortgage process a couple of ways:

Digital asset verification: Many banks, credit unions, and brokerages connect to our secure digital asset verification services. To initiate digital asset verification, click the link in our document portal, search for your financial institution, and follow along. We may even be able to document your income via direct deposits to your bank and eliminate requests for pay stubs or W-2s. Done and done!

Traditional documentation: If one or more of your financial institutions don’t connect to the digital service (or if you prefer), we’ll ask you to share account statements covering the most recent 60 days (2 monthly statements or 1 quarterly statement). We’ll have you print a transaction history from your bank’s website for transactions after your last statement.

Do I need to tell you about accounts I don’t plan to use for the mortgage?

It depends. We must document any assets that will contribute to the money you’re using to buy your home — including any accounts through which funds will pass. But we also like to see “reserves” — money left over in savings after closing.

Larger “jumbo” loans and loans to purchase multi-family homes or investment properties commonly require reserves.

But even when reserves aren’t required, sharing extra assets is never bad. Your loan looks less risky if we can see that you haven’t emptied your change jar, rummaged through your sofa cushions, and drained every last cent to fund your purchase.

There are instances when we can skip documenting certain assets. We can live without that credit union account you got in high school that still has a $100 balance or an old stray 401k.

If in doubt, just ask! We’ll help work out the minimum number of assets we can document to get the job done.

Will transferring money between accounts cause problems?

It’s not a problem, but it’s extra paperwork. Every time you transfer funds from one account to another, we need to see both ends of the transfer — the withdrawal from the outgoing account and the deposit into the incoming account. We recommend keeping transfers to a minimum to eliminate extra paperwork.

And note: it’s okay to send funds for closing from more than one account, so it isn’t necessary to consolidate accounts.

What if I co-own a bank account with someone who is not on the loan?

That’s okay! A few loan programs require a “joint access letter” — essentially a permission slip from any account owners who aren’t on the loan stating that you have access to the funds. We’ll help with the wording for this letter if it’s required.

Why do you need multiple months of bank statements?

Because Fannie Mae said so. (And don’t ask your father Freddie Mac. The answer’s still the same.) I’m kidding. Kind of. This requirement is an underwriting rule that’s standardized across most loan programs. The only exceptions are a few off-the-beaten-track (and expensive) “non-QM” loans.

Why are you asking about deposits to my bank account?

We must tally up your assets and document enough money to close. Any deposit exceeding 50% of your qualifying income triggers a requirement to document the source of funds. Our goal is to answer two questions:

Did the deposit come from a permitted source?

Most places your money could come from are allowed, so let’s be efficient and talk about what isn’t okay:

• Unsecured loans — A credit card advance, personal loan, or other borrowed funds not tied to an asset of equal or greater value.

• Untraceable funds — Cryptocurrency from a cold wallet and cash (green dollar bills).

• (Situationally) Gift funds — Gifts aren’t allowed for investment property purchases; some loans allow gifts after a specific minimum contribution from your funds.

Did the deposit come from a loan?

Funds from a secured loan are permitted — you can borrow from a home equity line of credit (HELOC), your 401k, or even take out a car title loan. However, a new debt might mean a new payment, we have to include in your debt-to-income ratio (DTI). We can ignore any payment on loans secured to financial assets like your 401k or a brokerage account. But we’ll add the payment for a credit card advance, draw from a HELOC, or a new car loan to your DTI.

Why are you asking for all the pages of my bank statements, brokerage statements, tax returns, and legal documents?

If a page on a bank, credit union, brokerage, or investment account is numbered, we need it – even if it’s blank or seems unimportant (even if it says “this page is intentionally blank”).

Tax returns and legal documents like divorce decrees, bankruptcy, or trust documents are also generally an all-or-nothing proposition. If required for your loan, we’ll ask you to provide every page.

Underwriters are like cats – a closed door drives them crazy (even if nothing is interesting on the other side). You know that the last page of your bank statement is blank, but they don’t until they see it.

How do I document the sale of a non-financial asset?

If you sell a non-financial asset like a car, boat, art, precious metals, or other personal property, we must document five things:

• Your ownership

• The value

• The sale

• Receipt of the funds

• The deposit your bank account

For the sale of a car or motorcycle, the paperwork looks like this:

• Copy of title (ownership)

• NADA or Kelley Blue Book printout (value)

• Bill of sale (sale)

• Check (not cash!) from the buyer (receipt of funds)

• Bank transaction history showing the deposit (deposit)

Sometimes, we have to get creative to check these boxes. A will, insurance policy, or old receipt could prove ownership. An appraisal, comparable item recently sold on eBay, or dealer’s valuation could document value. You get the idea.

Can I use cryptocurrency to pay my down payment?

Yup! The majority of loan programs allow cryptocurrency as a source of funds for closing, provided we document:

• The funds originated from an account in your name

• You exchange the funds into U.S. dollars before closing

So long as your chosen crypto exchange can generate a statement showing your name, we should be good to go.

Can you use cash as an asset, or does it have to be in the bank?

Cash held in green dollar bills generally can’t be used to cover your down payment or other purchase costs. We need to document your funds for closing – cash is tough to paper trail.

If we plan a few months ahead, you may have time to deposit cash and let it “season” in a bank account. But once you have an accepted offer, a cash deposit won’t count toward funds for closing and may cause other headaches.

The best things to do with your cash on hand are:

• Spend it on everyday expenses. Buy groceries and gas, pay rent and other bills so that paychecks and other traceable funds grow in your bank account.

• Hang onto it. A new home brings new expenses. Save your cash for the move, new appliances, furniture, and fixes to your new home. Or keep it around as an emergency fund.

Can I get a loan from my family for my down payment?

Nope. An unsecured loan — even from family — is never allowed as a source of funds for closing.

But if your family is feeling generous and wants to help out, there are three other options:

Gift

Gifts are allowed almost universally. We’ll document receipt of the funds and have you and your gift donor sign a letter stating that the funds are a gift with no expectation of repayment.

Secured loan

Borrowed funds are allowed if secured to an asset of equal or greater value. If you own another property, brokerage account, or any other asset worth the amount you’re borrowing, those assets can serve as collateral for a personal loan. If you’re putting at least 5% down from other funds, your family’s loan can be a second mortgage on the home you’re buying.

Non-borrowing co-purchaser

When family helps with a home purchase, their contribution often falls somewhere between a loan and a gift—no interest or payments, just a plan to repay someday, maybe after selling. If your family’s offer to help falls into this grey area, adding them as a co-purchaser may make sense. If they sign the purchase agreement and take title with you, their contribution simply counts as part of the down payment. We’ll document it like any other funds you’re using to close.

Keep us posted on your plans, and we’ll work with you and your family to find the option (or combination of options) that best fits everybody’s plans and goals.

Processing: Credit & Debts

What is a credit supplement?

A credit supplement (or “supp”) is how we update your credit report if information is missing, needs clarification, or requires correction. We order it through our credit reporting agency, Informative Research (IR).

But there’s a catch: creditors often won’t provide updates without your permission. That means a credit supp usually involves a three-way call between you, IR, and the creditor.

Three-way call for a credit supp kind of sucks. (I’m just telling it like it is.) You’re gonna jam out to some terrible hold music. So brew some tea, take a deep breath, and power through.

Hang in there, and thank you in advance. We only use this option when it’s absolutely necessary.

Pro Tip: The most common reason we need a credit supplement is to confirm you’ve paid off a debt. If your loan requires you paying a debt to qualify, we strongly recommend paying debts through closing. The settlement agent can collect funds and pay for you – and no tedious credit supp is required.

Why are you asking about inquiries on my credit report?

If your credit report reflects any recent inquiries, we’ll ask you to explain each and tell us if it resulted in a new account.

There can be a significant lag between applying for a new account and when it shows up on your credit report. We must include all your debts – even brand new ones – in your debt-to-income ratio.

Here’s what we’ll need:

• If you opened a new account: Documentation showing the amount you owe and the minimum monthly payment.

• If you opened an account but haven’t used it: A printout, statement, or letter from the creditor confirming the account has a zero balance.

• If no account was opened: A brief, signed note from you explaining the inquiry and confirming no new credit was issued.

Why are my credit card balances wrong?

The balances on your application come from our most recent credit report. Most creditors report to the credit bureaus monthly when they issue your bill. The balance on your mortgage application likely matches the last bill before we pulled up your credit report.

Can I use my credit cards?

Yup, you sure can! But a few words to the wise…

• Status quo is your friend. Sticking to your usual credit card usage patterns should preserve your credit scores and maintain a similar minimum payment.

• Don’t open any new credit cards. No matter how tempting a new air miles card looks, please hold off on opening new accounts until after the loan closes and keys are in your pocket.

• Keep credit use low. Next to paying on time, the best way to protect your credit is to keep credit cards at the same or lower balance. The ideal balance is below 30% of your credit limit.

You told me not to make “large purchases” — what counts as a large purchase?

It’s best to hold off on large purchases between getting your offer accepted and closing. But what counts as “large” depends on your financial resources and the funds required to close.

Even a major purchase (like a car) may not be a problem if you have a significant amount of extra cash. But if funds are very tight, even a big grocery run could cut into funds we were counting on to cover your down payment, closing cost, and “reserves” (the money you have left over in savings after closing).

If you’re considering a large purchase, please talk to us first. We’ll verify the spending you’re contemplating won’t negatively impact your loan.

Explore our PDF library…

We have a library of downloadable PDFs, explaining some of the more mystifying parts of the mortgage process.

These six are very relevant to the processing phase. Help Us Help You is full of protips for a drama-free transaction, so be sure to download that one, or head over to the page itself.